The Close Operating Model: Why Speed Without Structure Always Breaks

What high-performing teams know that most close improvement efforts miss

Finance teams have been trying to shorten the close for years.

Tools have improved. Automation has expanded. Checklists have multiplied. And yet, for most mid-market organizations, the close still runs longer than it should, still produces last-minute adjustments, and still depends on the same people doing heroic work at the end of every period.

The problem isn’t effort. It’s the model underneath the effort.

What most close improvement efforts get wrong

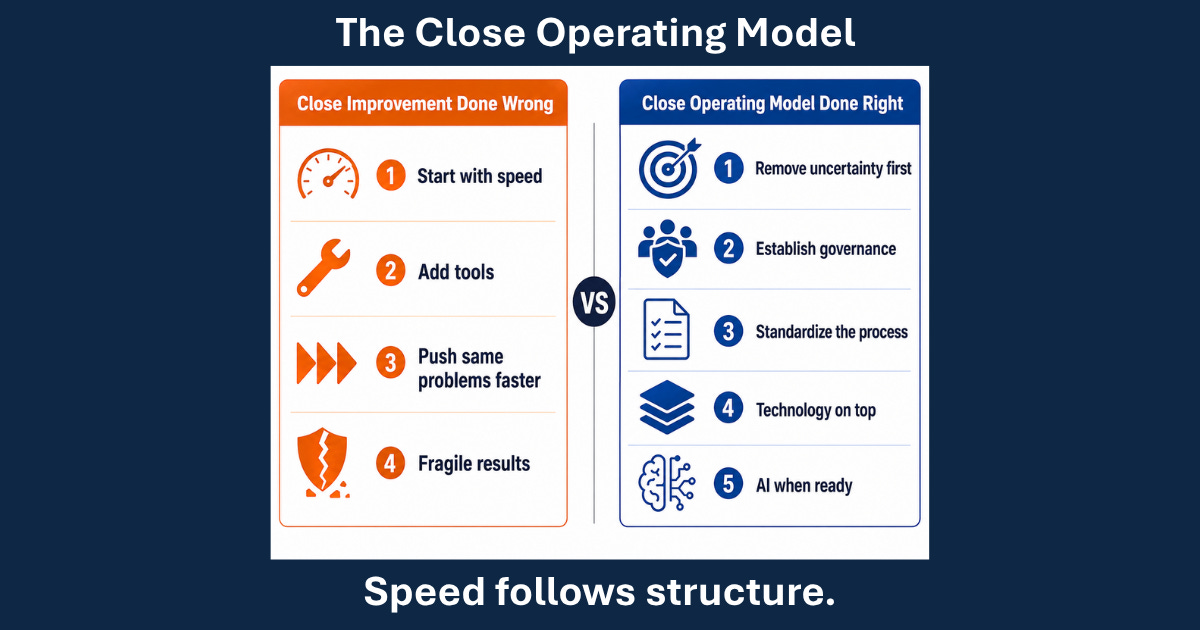

When organizations decide to improve the close, they usually start with speed. How do we cut days? Where are the bottlenecks? What can we automate?

Those are reasonable questions. But they’re the wrong starting point.

Close delays are rarely a capacity problem. They’re an uncertainty problem.

The close slows down when questions surface that should have been answered earlier. When ownership isn’t clear until something breaks. When data arrives unreconciled and has to be cleaned during the close window. When every period feels like the first time the team has done this.

Chasing speed in that environment doesn’t improve the close. It compresses the chaos into a shorter window.

The teams that actually improve the close start by removing uncertainty — not by cutting time.

What a close operating model actually requires

A close operating model is not a checklist. It’s not a set of deadlines. It’s not a dashboard that shows which tasks are green and which are red.

It’s a governed, repeatable framework for how the close runs — every period, across every team, with clear ownership, defined standards, and visibility into where things stand before they become problems.

Three things have to be in place for that to work.

Governance. Someone has to own the close as an enterprise process. Not just within accounting. Across every function that feeds into it. Without a clear owner — ideally a Controller-led structure with process owners embedded in each team — escalation stays ad hoc and standards don’t hold.

Standardization. Every team running the close differently creates friction. Different cutoff interpretations. Different reconciliation formats. Different expectations for what “complete” means. Standardization doesn’t mean rigidity. It means consistency — so that each period builds on the last instead of starting from scratch.

Technology that enables, not just organizes. Most organizations have an ERP. Most organizations also need something beyond it — close management tools, reconciliation platforms, workflow systems — to actually automate the process and create the visibility that the ERP alone doesn’t provide. Without that layer, even the best governance structure runs on spreadsheets and email.

The AI problem hiding inside the close

Here’s where it gets more urgent.

Organizations are beginning to introduce AI into the close. Variance explanations. Anomaly detection. First-pass journal entries. These are real capabilities that are already available.

But AI in the close only works if the process underneath it is consistent.

AI can’t reconcile definitions that the organization hasn’t agreed on. It can’t flag anomalies reliably when the baseline keeps shifting. It can’t produce audit-ready outputs when the controls aren’t designed for automation.

The teams that are positioned to benefit from AI in the close are the ones that have already built the operating model. Not because AI requires perfection — but because AI amplifies whatever it lands on. Consistent process gets better. Inconsistent process gets amplified.

That’s the sequence that matters: operating model first, AI second.

Where mid-market teams have an advantage

Large enterprises face a significant challenge in close transformation. Legacy systems, siloed teams, and years of workarounds have calcified into the way things are done. Changing it requires multi-year programs and significant organizational change management.

Mid-market teams have a genuine structural advantage.

Fewer layers means governance is simpler to establish. Closer relationships between accounting and operations means alignment is more direct. Shorter feedback loops means you can standardize faster and see results sooner.

The opportunity isn’t to replicate what large enterprises do. It’s to build the operating model correctly before the organization gets complicated enough to make it hard.

What to do with this

If your close is running longer than it should — or if it’s technically fast but producing adjustments you keep discovering after the fact — the issue is almost certainly in the operating model, not the timeline.

The starting point is a clear-eyed look at three things:

Where does uncertainty enter the close? What questions surface late that should have been answered earlier?

Where is ownership unclear? Which handoffs between teams create the most friction?

Where is the technology running the process vs. where is the process running around the technology?

Those three questions will tell you more about your close than any benchmarking exercise.

Speed follows structure. Not the other way around.